Calculates the number of days between the last coupon payment date and the settlement date for a fixed-income security with regular interest payments.

Syntax

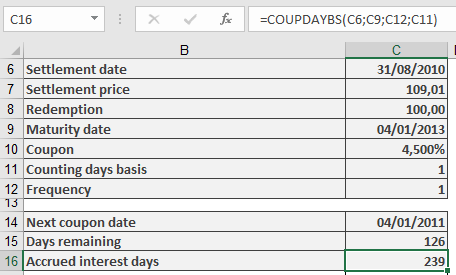

COUPDAYBS(Settlement; Maturity; Frequency; Basis)

Arguments

| Argument | Required | Description | Valid Values |

| Settlement | Yes | Date of ownership transfer | Valid date format |

| Maturity | Yes | Bond repayment date | Must be after Settlement |

| Frequency | Yes | Interest payments per year | 1 (annual), 2 (semi-annual), 4 (quarterly) |

| Basis | No | Day-count convention (see Table 1) | 0-4 (default=0) |

Day-Count Basis Methods (Table 1)

| Basis | Method | Description |

| 0 | 30/360 (NASD) | 30-day months, 360-day year |

| 1 | Actual/Actual | Exact calendar days |

| 2 | Actual/360 | Actual days/360-day year |

| 3 | Actual/365 | Actual days/365-day year |

| 4 | 30/360 (European) | European 30-day convention |

Requirements & Error Handling

- Dates must be valid (no time component)

- Frequency and Basis are truncated to integers

- Returns #VALUE! for invalid dates

- Returns #NUM! for:

- Invalid Frequency (≠1,2,4)

- Invalid Basis (≠0-4)

- Settlement date > Maturity date

Background

- Used to calculate accrued interest owed when bonds trade between coupon dates

- Different day-count methods yield slightly different results

- Essential for accurate bond pricing and yield calculations

Example Applications

- Accrued Interest Calculation:

Accrued Interest = (Annual Coupon Rate × Face Value) × (COUPDAYBS()/Days in Coupon Period)

- Yield Analysis:

- Used with YIELD() and PRICE() functions

- Helps determine exact holding period returns

Key Notes

- For US corporate bonds: Typically Basis=0 (30/360)

- For government bonds: Typically Basis=1 (Actual/Actual)

- Always verify Settlement < Maturity

- Combine with COUPNCD() and COUPPCD() for complete coupon date analysis