Calculates the number of days from the settlement date to the next coupon payment date for a fixed-income security.

Syntax

COUPDAYSNC(Settlement; Maturity; Frequency; Basis)

Arguments

| Argument | Required | Description | Valid Values |

| Settlement | Yes | Date ownership transfers | Valid date (time truncated) |

| Maturity | Yes | Bond repayment date | Must be after Settlement |

| Frequency | Yes | Coupon payments per year | 1, 2, or 4 |

| Basis | No | Day-count method | 0-4 (default=0) |

Day-Count Basis Methods

| Basis | Method | Key Characteristic |

| 0 | 30/360 (NASD) | Standard financial convention |

| 1 | Actual/Actual | Exact day count |

| 2 | Actual/360 | Money market convention |

| 3 | Actual/365 | British convention |

| 4 | 30/360 (European) | Eurobond convention |

Key Features

- Primary Use:

- Determines days until next coupon payment

- Essential for calculating:

- Accrued interest allocations

- Present value of future cash flows

- Error Handling:

- #VALUE!: Invalid date format

- #NUM!:

- Invalid Frequency/Basis

- Settlement ≥ Maturity

- Calculation Method:

- Automatically identifies next coupon date

- Applies specified day-count convention

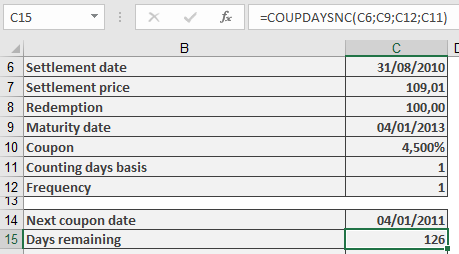

EXAMPLE

Common Implementation Errors

- Using maturity date as settlement

- Incorrect Basis for security type

- Forgetting to truncate time values