Calculates the effective annual interest rate (compounded) from a nominal annual rate, accounting for intra-year compounding periods.

Syntax

EFFECT(Nominal_Interest; Periods)

Arguments

- Nominal_Interest (required)

The stated annual nominal interest rate (e.g., 0.05 for 5%). Must be > 0. - Periods (required)

The number of compounding periods per year (e.g., 12 for monthly). Must be ≥ 1 (decimal places truncated).

Error Handling

- #VALUE! if non-numeric inputs are provided.

- #NUMBER! if:

- Nominal_Interest ≤ 0.

- Periods < 1.

Background

- Nominal vs. Effective Rates:

- Nominal rates ignore compounding (e.g., 5% annual, paid monthly = 5%/12 per period).

- Effective rates reflect actual annual yield after compounding (e.g., 5% nominal → ~5.12% effective for monthly compounding).

- Formula:

Examples

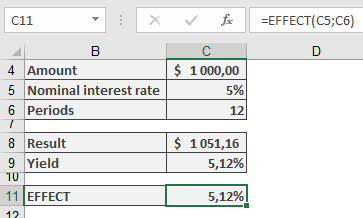

- Savings Account

- Scenario: $1,000 deposited at 5% nominal interest, compounded monthly.

- Calculation:

=EFFECT(5%, 12) → Returns **5.12%**

-

- Verification:

- Monthly interest: 5%/12 = 0.4167%.

- Year-end balance: =FV(5%/12, 12, , -1000) = $1,051.16.

- Effective yield: (1051.16 / 1000) – 1 = 5.12%.

- Verification:

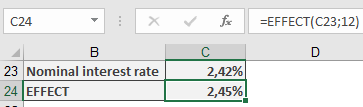

- Mortgage Loan

- Scenario: Bank offers 2.42% nominal rate, compounded monthly.

- Calculation:

=EFFECT(2.42%, 12) → Returns **2.45%** (matches advertised effective rate).

-

- Note: Banks may use alternative methods; exact matches may be coincidental.

Key Points

- Comparison Tool: Use to compare loans/investments with different compounding frequencies.

- Limitations: Assumes reinvestment at the same rate; does not account for fees or irregular payments.