Its calculates the equivalent annual interest rate (in arrears) for a discounted security (e.g., zero-coupon bond) with intra-year maturity.

Syntax

INTRATE(Settlement; Maturity; Investment; Repayment; [Basis])

Arguments

| Argument | Description |

| Settlement (required) | Purchase date of the security (time truncated). |

| Maturity (required) | Maturity/redemption date (time truncated). |

| Investment (required) | Purchase price (must be > 0). |

| Repayment (required) | Redemption value at maturity (must be > 0). |

| Basis (optional) | Day-count convention (see Table 15-2). Default: 0 (US 30/360). |

Error Handling

- #VALUE! → Invalid dates or non-numeric inputs.

- #NUMBER! → If:

- Investment ≤ 0 or Repayment ≤ 0.

- Basis < 0 or > 4.

- Settlement ≥ Maturity.

Background

- Anticipative vs. Arrears Yield:

- Anticipative (DISC): Interest deducted upfront (e.g., T-bills).

- Arrears (INTRATE): Interest paid at maturity (converted to annual equivalent).

- Formula:

- Comparison: Use to contrast with fixed-income securities paying periodic interest.

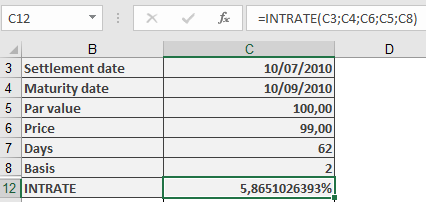

Example

Treasury Bill (T-Bill) Calculation

- Purchase Date: 10, 07, 2010

- Maturity: 10, 09, 2010

- Purchase Price (Investment): $99

- BASIS: 2

- Par Value: 100

=INTRATE(« 10/09/2010 », « 10/09/2010 », 99, 100, 2)

Result: 5.87% annual yield.

Key Notes

- No Compounding: Simple interest only.

- Inverse of DISC(): Converts discount rate to equivalent annual yield.

- Use Case: Compare short-term securities (e.g., commercial paper, T-bills).