This function calculates the modified internal rate of return (MIRR), evaluating negative cash flows (disbursements) and positive cash flows (deposits) at different interest rates.

Syntax:

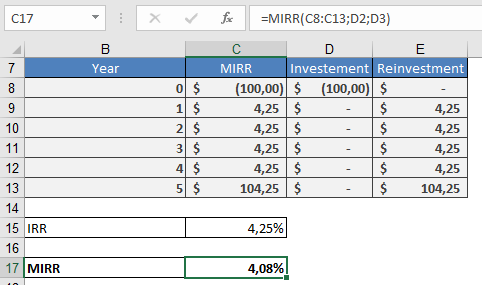

MIRR(Values; Investment; Reinvestment)

Arguments

- Values (required)

- A range of cash flows (disbursements and deposits) arranged chronologically.

- Each value represents the end of a period (e.g., yearly).

- Must include at least one positive and one negative value.

- Non-numeric or empty cells are ignored.

- Investment (required)

- The discount rate applied to negative cash flows (borrowing cost).

- Reinvestment (required)

- The interest rate applied to positive cash flows (reinvestment yield).

Background

The MIRR method improves upon the standard IRR() by:

- Separate rates for financing (negative flows) and reinvestment (positive flows).

- Eliminating multiple IRR issues that arise with irregular cash flows.

- Providing a realistic reinvestment assumption (unlike IRR, which assumes reinvestment at the IRR itself).

Advantages:

✔ Clear reinvestment rate – Reflects realistic earnings on deposits.

✔ No time horizon limitation – Unlike NPV, which requires a fixed rate.

Disadvantages:

✖ Fixed rates – Assumes constant borrowing and reinvestment rates.

Example

An investor buys a 5-year government bond with:

- Annual coupon rate: 4.25%

- Reinvestment rate: 2% (due to market conditions)

IRR vs. MIRR:

| Metric | Calculation | Result |

| IRR() | Standard return | 4.25% |

| MIRR() | Adjusted for reinvestment | 4.08% |

Interpretation:

- Initial investment: $100

- Future value (FV):

- Coupons reinvested at 2% → $122.12 after 5 years.

- MIRR (4.08%) reflects the true annualized return after accounting for lower reinvestment yields.

Key Takeaway

MIRR provides a more realistic measure of profitability by:

- Using separate rates for costs and reinvestment.

- Avoiding the overstated returns of IRR when reinvestment rates differ.