Calculates the price of a fixed-interest security, accounting for a first interest period that is either shorter or longer than subsequent regular periods (quarterly, semi-annual, or annual).

Syntax

ODDFPRICE(Settlement; Maturity; Issue; First_Interest_Date; Rate; Yield; Repayment; Frequency; [Basis])

Arguments

- Settlement (required) – The date the security is transferred to the buyer.

- Maturity (required) – The date the security’s principal is repaid.

- Issue (required) – The issuance date of the security.

- First_Interest_Date (required) – The date of the first interest payment.

- Rate (required) – The bond’s nominal annual interest rate (coupon rate).

- Yield (required) – The market yield for bonds of the same maturity.

- Repayment (required) – The redemption value per 100 units of par value.

- Frequency (required) – Number of interest payments per year (1 = annual, 2 = semi-annual, 4 = quarterly).

- Basis (optional) – Day-count convention . Defaults to 0 if omitted.

Notes

- Dates must be entered without time values; decimals are truncated.

- Frequency and Basis are truncated to integers.

- If dates are invalid, #VALUE! is returned.

- Yield and Repayment must be non-negative; otherwise, #NUM! is returned.

- If Frequency is not 1, 2, or 4, or Basis is outside 0–4, #NUM! is returned.

- The chronological order must be:

Maturity > First_Interest_Date > Settlement > Issue; otherwise, #NUM! is returned.

Background

The function applies the financial principle:

Creditor’s Payment = Debtor’s Payment

At the transaction’s start, the security’s price plus accrued interest equals the present value of future cash flows (interest + principal). The price is expressed as a percentage of par (e.g., 100 units).

Calculating present value is straightforward if:

- The settlement coincides with an interest payment date, and

- Interest is paid annually.

However, complexities arise with:

- Settlement between interest dates, or

- Multiple annual payments.

Finance mathematics uses various methods (e.g., Moosmüller, Braess/Fangmeyer, ISMA) to handle partial periods. For ISMA compatibility with Excel, see the PRICE() and YIELD() background notes.

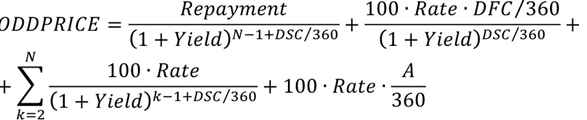

Formula (Simplified Case)

For annual payments (360-day year) and a shortened first period, the formula in Excel Help reduces to:

Formula variables:

- N = Total interest periods,

- A = Days from issue to settlement,

- DSC = Days from settlement to first interest date,

- DFC = Days from first interest date to maturity.]

Unlike PRICE(), the first period is treated separately (not summed with others) because its coupon is partial.

For Frequency > 1, Rate and Yield are adjusted for intra-year periods.

For lengthened first periods, the formula accounts for hypothetical interim interest payments realized at the period’s end. Accrued interest is handled similarly.

Note: The function is irrelevant once the first interest date passes.

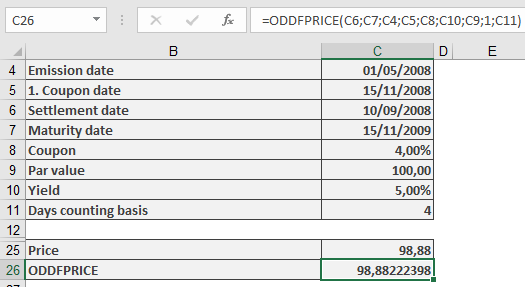

Example

The sample files include a fictitious bond calculation with a shortened first interest period. The result aligns with ODDFPRICE()‘s output.