Its calculates the yield of a fixed-interest security from the settlement date to maturity, accounting for a first interest period that may be shorter or longer than subsequent regular periods.

Syntax

ODDFYIELD(Settlement; Maturity; Issue; First_Interest_Date; Rate; Price; Repayment; Frequency; [Basis])

Arguments

- Settlement (required) – The date the bond is transferred to the buyer.

- Maturity (required) – The date the bond’s principal is repaid.

- Issue (required) – The issuance date of the security.

- First_Interest_Date (required) – The date of the first interest payment.

- Rate (required) – The bond’s nominal annual interest rate (coupon rate).

- Price (required) – The bond’s price at settlement (as a percentage of par value, where par = 100).

- Repayment (required) – Redemption value per 100 units of par value.

- Frequency (required) – Interest payments per year (1 = annual, 2 = semi-annual, 4 = quarterly).

- Basis (optional) – Day-count convention. Defaults to 0 if omitted.

Notes

- Dates must be entered without time values; decimals are truncated.

- Frequency and Basis are truncated to integers.

- Invalid dates return #VALUE!.

- Price and Yield must be non-negative; otherwise, #NUM! is returned.

- If Frequency is not 1, 2, or 4, or Basis is outside 0–4, #NUM! is returned.

- Chronological order must be:

Maturity > First_Interest_Date > Settlement > Issue; otherwise, #NUM! is returned.

Background

For theoretical details, refer to the ODDFPRICE() function background.

ODDFYIELD() computes the effective yield required for a bond to reach its market price, informing investors of the expected return. The calculation mirrors ODDFPRICE() but solves for yield instead of price.

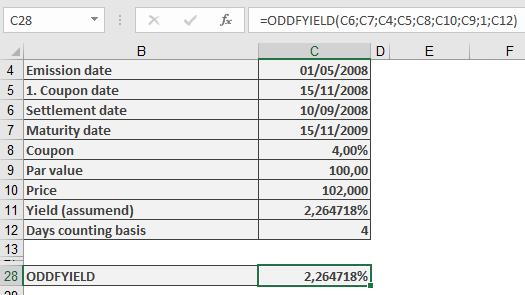

Example

The sample files include a fictitious bond with a shortened first interest period, The yield is derived iteratively (via goal-seek) to match the target price. ODDFYIELD() returns identical results.