Its calculates the price of a fixed-interest security with a final interest period that differs in length from previous regular periods, without considering compound interest.

Syntax

ODDLPRICE(Settlement; Maturity; Last_Interest_Date; Rate; Yield; Repayment; Frequency; [Basis])

Arguments

- Settlement (required): Date when ownership of the bond transfers to buyer

- Maturity (required): Date when principal repayment occurs

- Last_Interest_Date (required): Date of last regular interest payment

- Rate (required): Bond’s nominal annual interest rate (coupon rate)

- Yield (required): Market interest rate for bonds of equivalent duration

- Repayment (required): Redemption value as percentage of par value (where par = 100)

- Frequency (required): Interest payments per year (1=annual, 2=semi-annual, 4=quarterly)

- Basis (optional): Day-count convention (see Table 15-2). Defaults to 0 if omitted.

Notes

- Date inputs must not include time values; decimal places are truncated

- Frequency and Basis are converted to integers

- Invalid dates return #NUM! error

- Rate and Yield must be non-negative; otherwise returns #NUM!

- Returns #NUM! if:

- Frequency is not 1, 2, or 4

- Basis is outside 0-4 range

- Chronological order is violated: Maturity > Settlement > Last_Interest_Date

Background

The function applies the financial principle:

Creditor’s Payment = Debtor’s Payment

At transaction initiation:

- Security price + accrued interest = Present value of future cash flows

- Price is expressed as percentage of par value (100 units)

Calculation is straightforward when:

- Settlement coincides with interest payment date, and

- Interest is paid annually

Complexities arise when:

- Settlement occurs between interest dates, or

- Multiple annual payments exist

Common financial methods for partial periods include:

- Moosmüller

- Braess/Fangmeyer

- ISMA (see PRICE() and YIELD() background for Excel-ISMA correlation)

Calculation Method

Excel uses simple yield (no compounding) with these principles:

- Accrued interest calculated from days since last interest payment

- Partial yield derived from days to maturity (based on year length)

- Only applicable during final period before maturity

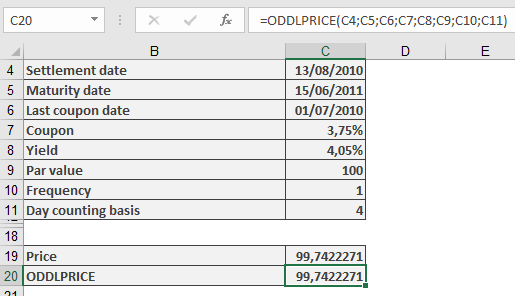

Example

Sample files include a fictitious bond calculation matching the logic, demonstrating:

- Terms with irregular final period

- Price calculation methodology

- Identical results to ODDLPRICE() function output