Its calculates the yield of a fixed-interest security with an irregular final interest period (different length from previous regular periods), using simple interest (no compounding).

Syntax

ODDLYIELD(Settlement; Maturity; Last_Interest_Date; Rate; Price; Repayment; Frequency; [Basis])

Arguments

| Parameter | Requirement | Description |

| Settlement | Required | Date of bond ownership transfer |

| Maturity | Required | Date of principal repayment |

| Last_Interest_Date | Required | Date of last regular interest payment before purchase |

| Rate | Required | Nominal annual interest rate (coupon rate) |

| Price | Required | Bond price as percentage of par value (par = 100) |

| Repayment | Required | Redemption value percentage (per 100 par value) |

| Frequency | Required | Annual payment frequency (1, 2, or 4) |

| [Basis] | Optional | Day-count convention (0-4, default=0) |

Validation Rules

- Date Handling:

- Time values are ignored (truncated)

- Invalid dates return #NUM! error

- Required sequence: Maturity > Settlement > Last_Interest_Date

- Numerical Requirements:

- Rate ≥ 0, Price ≥ 0 (else #NUM!)

- Frequency ∈ {1,2,4}

- Basis ∈ {0,1,2,3,4}

Background

This function complements ODDLPRICE(), calculating the effective yield needed to achieve a specified market price. It uses simple yield methodology (no compounding) where:

- Annual yield is derived from partial period calculations

- Interest at maturity includes accruals since last payment date

- Accrued interest is prorated based on time elapsed

Calculation Method

The yield is determined by:

- Solving the price formula for yield

- Annualizing partial period results

- Prorating interest between last payment and settlement

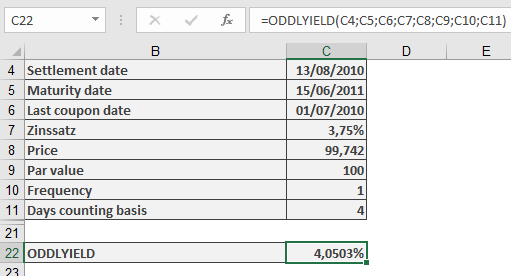

Example

Sample files demonstrate calculation for bonds with irregular final periods:

Error Conditions

| Error | Trigger Condition |

| #NUM! | Invalid dates, negative values, or parameter constraints violated |

| #VALUE! | Non-numeric arguments |

Note

Function is only applicable during the final irregular period before maturity.