Its calculates the net present value (NPV) of a series of cash flows occurring at irregular intervals, discounted at a specified annual rate. Unlike standard NPV, XNPV uses exact dates for precise time-adjusted valuation.

Syntax

XNPV(Rate; Values; Dates)

Arguments

| Argument | Required | Description | Validation Rules |

| Rate | Yes | Annual discount rate (e.g., 10% = 0.10). | Must be numeric. |

| Values | Yes | Array of cash flows: • Negative: Outflows (costs) • Positive: Inflows (income). |

Must include ≥1 positive and ≥1 negative value. |

| Dates | Yes | Exact dates corresponding to each cash flow. | Dates must align with Values array; first date = start point. |

Error Conditions

- #VALUE!: Invalid date format.

- #NUM!: If:

• Dates/Values arrays mismatch in size

• All cash flows are positive/negative

• Dates are non-chronological.

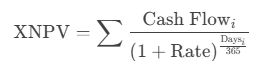

Key Formula

Where Days = Exact days from the first date in the series.

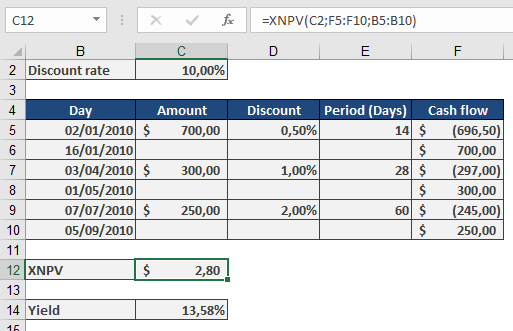

Example: Evaluating Discount Terms

Scenario:

A dealer offers payment terms with discounts for early payment. Compare against a 10% annual investment yield.

Cash Flows:

Calculation:

Effective Yield (XIRR Verification):

=XIRR({-696.5, -297, -245, 700, 300, 250}, {« 1/2/2010 », « 4/3/2010 », « 7/7/2010 », « 1/16/2010 », « 5/1/2010 », « 9/7/2010 »})

Result: 13.58% (beats 10% alternative).

Why Use XNPV?

- Precision: Accounts for exact days between cash flows (e.g., 14 days vs. « 1 month »).

- Flexibility: Evaluates irregular income/expenditures (e.g., project milestones, custom payment plans).

- Decision Tool:

- Positive NPV: Project/investment adds value.

- Negative NPV: Reconsider or adjust terms.

Comparison with NPV

| Feature | XNPV | NPV |

| Timing | Exact dates | Equal intervals |

| Formula | Daily compounding (365) | Periodic compounding |

| Use Case | Leases, trade credit | Annuities, loans |