Its calculates the annual yield of a fixed-interest security (bond) given its price, coupon rate, and maturity date. This represents the effective return an investor would earn if the bond is held to maturity.

Syntax

YIELD(Settlement; Maturity; Rate; Price; Redemption; Frequency; [Basis])

Arguments

| Argument | Required | Description | Validation Rules |

| Settlement | Yes | Bond purchase date. | Must be valid date < Maturity. |

| Maturity | Yes | Bond maturity/redemption date. | Must be valid date > Settlement. |

| Rate | Yes | Annual coupon rate (decimal). | ≥ 0 (e.g., 5% = 0.05). |

| Price | Yes | Bond price per $100 face value. | > 0 (e.g., 95.50 for $95.50). |

| Redemption | Yes | Redemption value per $100 face value. | Typically 100. |

| Frequency | Yes | Coupon payments per year: 1 = Annual 2 = Semi-annual 4 = Quarterly. |

∈ {1, 2, 4}. |

| [Basis] | No | Day-count convention (0-4). Default=0. | See Table 15-2. |

Error Conditions

- #VALUE!: Invalid dates.

- #NUM!: If:

• Rate < 0 or Price ≤ 0

• Frequency ∉ {1, 2, 4}

• Basis ∉ {0, 1, 2, 3, 4}

• Settlement ≥ Maturity.

Key Formula

Solves for Yield (y) in:

Where:

- f = Frequency

- k = Period number

- N = Total periods

Examples

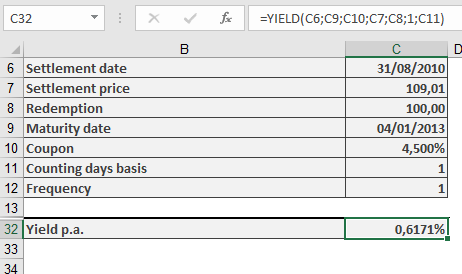

- Annual Coupon Bond

Scenario:

- Settlement: 31-Aug-2010

- Maturity: 4-Jan-2013

- Coupon Rate: 4.5%

- Price: $109.01 (per $100 face value)

- Redemption: $100

- Frequency: 1 (annual)

- Basis: 1 (Actual/actual)

Calculation:

=YIELD(« 8/31/2010 », « 1/4/2013 », 0.045, 109.01, 100, 1, 1)

Result: 0.617% annual yield.

ISMA Yield Conversion:

=EFFECT(YIELD(…), 2)

Background

- Day-Count Conventions:

| Basis | Method |

| 0 | US (NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

- Yield Types:

- Current Yield: Coupon/Price (simpler but less accurate).

- Yield to Maturity (YTM): Total return (what YIELD() calculates).

- Market Dynamics:

- Price < 100 → Yield > Coupon Rate (discount bond).

- Price > 100 → Yield < Coupon Rate (premium bond).