Calculates the future value of an investment or loan based on periodic, constant payments and a constant interest rate.

Syntax

FV(Rate; Nper; Pmt; [Pv]; [Type])

Arguments

- Rate (required)

The interest rate per period (e.g., 4.5% annual → 4.5%/12 for monthly). - Nper (required)

The total number of payment periods (e.g., 15 years × 12 months = 180). - Pmt (optional)

The regular payment per period (annuity). Use 0 if omitted.- Sign Convention:

- Negative (-): Cash outflow (e.g., deposits, loan payments).

- Positive (+): Cash inflow (e.g., withdrawals, dividends).

- Sign Convention:

- Pv (optional)

The present value (initial lump sum). Defaults to 0. - Type (optional)

- 0 (default): Payments at end of period (ordinary annuity).

- 1: Payments at start of period (annuity due).

Error Handling

- Ensure Rate, Nper, Pmt, and Pv are numeric to avoid #VALUE!.

- Nper must be ≥ 1.

Background

FV() solves the time value of money equation:

Examples

- Compound Interest (Lump Sum)

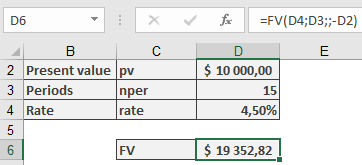

- Scenario: $10,000 invested at 4.5% annual interest for 15 years.

- Formula:

=FV(4.5%, 15, , -10000) → **$19,352.82**

-

- Note: Pv is negative (cash outflow).

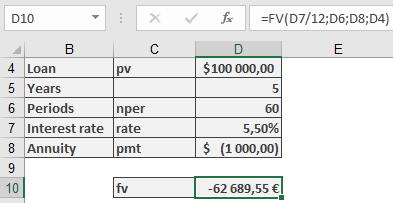

- Loan Repayment (Residual Debt)

- Scenario: $100,000 loan at 5.5% annual interest, $1,000 monthly payments for 5 years.

- Formula:

=FV(5.5%/12, 5*12, -1000, 100000) → **$62,689.55** (remaining balance)

Key Notes

- Sign Convention: Payments out are negative; inflows are positive.

- Compounding: For loans, interest is typically nominal (e.g., monthly rate = annual rate/12).

- Annuity Types: Type=1 for payments at period start (e.g., leases).