This function calculates the modified duration for fixed-interest securities.

Syntax:

MDURATION(Settlemen; Maturity; Nominal_Interest; Yield; Frequency; Basis)

Arguments:

- Settlement (required) – The date when ownership of the security is transferred.

- Maturity (required) – The date when the loan (represented by the security) is repaid.

- Nominal_Interest (required) – The annual coupon rate (agreed interest rate) of the security.

- Yield (required) – The market interest rate on the settlement date, used to discount future cash flows in the duration calculation.

- Frequency (required) – The number of interest payments per year. Valid options:

- 1 = Annual

- 2 = Semiannual

- 4 = Quarterly

- Basis (optional) – The day-count convention. If omitted, Excel defaults to Basis = 0.

Notes:

- Date arguments are truncated to integers (no time component).

- Frequency and Basis must be integers (decimal places are truncated).

- Errors:

- #VALUE! – Invalid dates or non-numeric inputs where required.

- #NUM! – Invalid numbers for non-date arguments.

Background:

Modified duration measures a bond’s price sensitivity to interest rate changes, crucial for risk management. Unlike stocks, fixed-income securities see reduced price volatility as maturity nears because redemption value is fixed.

Mathematically:

- Duration = Macaulay Duration (see DURATION()).

- MDURATION() returns the scaling factor for estimating relative price change due to interest rate shifts (unsigned).

- For multiple annual payments, the yield is distributed evenly across periods.

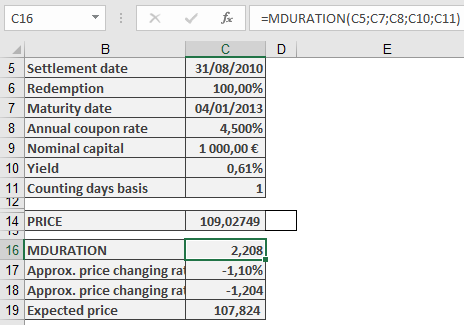

Example:

A 4.5% federal bond (issued 2003) had:

- Yield (Aug 31, 2010): 0.61%

- Maturity: Jan 4, 2030

- Price: $109.027

Scenario:

- If yield rises +0.5% (to 1.11%), the price drops to $107.800 (–1.13%).

Using MDURATION():

- Modified Duration = 2.208

- Estimated price change = 2.208 × 0.5% ≈ 1.1% decline

- New price ≈ $107.824 (vs. actual $107.800)

Conclusion:

Modified duration helps investors quickly assess risk without complex recalculations.