Calculates the periodic payment amount (annuity) for a loan or investment based on constant payments and a constant interest rate. For loan repayment calculations, this represents the fixed payment amount that includes both principal and interest.

Syntax

PMT(Rate; Nper; Pv; [Fv]; [Type])

Arguments

| Argument | Requirement | Description |

| Rate | Required | Periodic interest rate (typically annual rate divided by periods per year) |

| Nper | Required | Total number of payment periods |

| Pv | Required | Present value (loan amount or initial investment) |

| [Fv] | Optional | Future value (desired balance after last payment) |

| [Type] | Optional | Payment timing: 0=end of period (default), 1=beginning of period |

Note: Either Pv or Fv must be specified.

Background

The PMT() function is part of a financial function family that includes:

- PV() (present value)

- FV() (future value)

- NPER() (number of periods)

- RATE() (interest rate)

These functions are interrelated through the financial equation:

[Financial equation graphic showing relationship between PV, FV, PMT, NPER, RATE]

Where:

- All values are compounded

- M represents the Type parameter (payment timing)

- The equation is solved for each respective function

Examples

- Annuity Calculation (Retirement Planning)

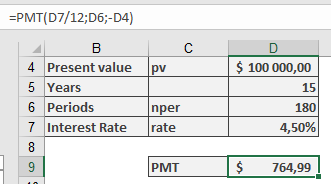

A 60-year-old has $100,000 saved and wants monthly payments for 15 years at 4.5% annual interest.

Scenario A: Exhaust all capital

=PMT(4.5%/12, 15*12, -100000)

Result: $764.99 per month

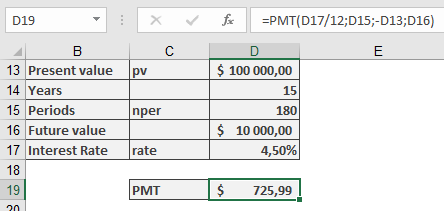

Scenario B: Maintain $10,000 balance

=PMT(4.5%/12, 15*12, -100000, 10000)

Result: $725.99 per month

Note: Negative Pv indicates outgoing payment (capital invested)

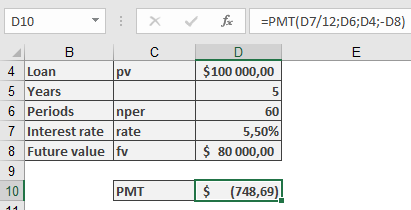

- Loan Repayment Calculation

$100,000 loan at 5.5% annual interest with 5-year term and $80,000 residual balance.

=PMT(5.5%/12, 5*12, 100000, -80000)

Result: $748.69 per month (negative indicates outgoing payment)

Key Differences:

- Savings calculations assume compound interest

- Mortgage loans typically use simple monthly interest (annual rate/12)

Important Notes

- For loans, payments are negative (cash outflow)

- Interest rates should match payment periods (annual rate/12 for monthly payments)

- Type parameter significantly affects beginning/end of period calculations

- Results are theoretical for accounts without true compound interest