Its calculates the present value of an investment based on a constant interest rate and a series of future payments (annuities) and/or a lump sum.

Syntax

PV(Rate; Nper; [Pmt]; [Fv]; [Type])

Arguments

| Argument | Requirement | Description | Financial Meaning |

| Rate | Required | Interest rate per period | Cost of capital/discount rate |

| Nper | Required | Total number of periods | Investment/loan term |

| [Pmt] | Conditionally Required | Payment per period | Annuity amount |

| [Fv] | Optional | Future value | Target balance/residual value |

| [Type] | Optional | Payment timing: 0 = end period (default) 1 = beginning period |

Cash flow timing |

Note: Either Pmt or Fv must be provided.

Financial Model

Implements the time value of money principle:

PV + Σ[Pmt/(1+Rate)^k] + Fv/(1+Rate)^Nper = 0

where k ranges from 1 to Nper (adjusted for Type).

Key Applications

- Lump Sum Investments (Retirement Planning)

=PV(Rate, Nper,, Fv)

- Annuity Valuation (Pension Planning)

=PV(Rate, Nper, Pmt)

- Loan Capacity (Mortgage Underwriting)

=PV(Rate, Nper, -Pmt)

Examples

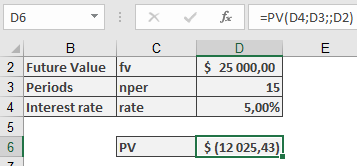

- Retirement Savings Verification

Scenario:

$10,000 invested for 15 years at 5% p.a. targeting $25,000.

Calculation:

=PV(5%, 15,, 25000)

Result: -$12,025.43

Interpretation: Requires $12,025 initial investment to reach target (current $10,000 insufficient).

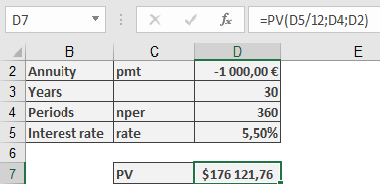

- Mortgage Qualification

Scenario:

$1,000 monthly payment capacity for 30 years at 5.5% p.a.

Calculation:

=PV(5.5%/12, 30*12, -1000)

Result: $176,121.76

Interpretation: Maximum loan amount at given terms.

Important Notes

- Sign Convention:

- Positive results = Cash inflows

- Negative results = Cash outflows

- Compounding Assumptions:

- For monthly payments, divide annual rate by 12

- For quarterly payments, divide annual rate by 4

- Precision Tip:

For loan amortization schedules, combine with ROUND():

=ROUND(PV(…), 2)