Its calculates the maturity value (redemption amount) for a fully discounted security that uses anticipative interest calculation (interest deducted upfront).

Syntax

RECEIVED(Settlement; Maturity; Investment; Discount; [Basis])

Arguments

| Argument | Required | Description | Validation Rules |

| Settlement | Yes | Trade settlement date | Must be valid date ≤ Maturity |

| Maturity | Yes | Security maturity date | Must be valid date ≥ Settlement |

| Investment | Yes | Amount invested (purchase price) | > 0 |

| Discount | Yes | Annual discount rate | > 0 |

| [Basis] | No | Day count convention (0-4) | Default=0 |

Error Conditions

- #VALUE!: Invalid dates or non-numeric inputs

- #NUM!: Negative amounts or invalid Basis

Key Features

- Anticipative Interest Model:

- Interest deducted at inception (discount instrument)

- Contrasts with standard arrears interest calculation

- Common Applications:

- Treasury bills

- Commercial paper

- Bankers’ acceptances

Calculation Method

Maturity Value = Investment / (1 – (Discount × DSM/DIM))

Where:

- DSM = Days from settlement to maturity

- DIM = Days in year per Basis convention

Examples

- Bill of Exchange

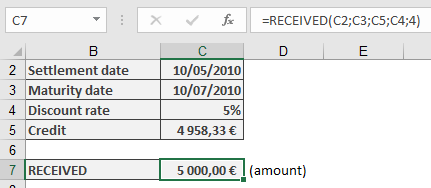

Scenario:

- Settlement: 10-May-2010

- Maturity: 10-Jul-2010 (2 months)

- Investment: $4,958.33

- Discount: 5% p.a.

- Basis: 4 (European 30/360)

Calculation:

=RECEIVED(« 5/10/2010″, »7/10/2010 »,4958.33,5%,4)

Result: $5,000.00

Face value of the bill

Important Notes

- Day Count Conventions:

| Basis | Method |

| 0 | US (NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

- Financial Context:

- Primarily for short-term instruments (<1 year)

- Represents the face value calculation

- Complementary to PRICEDISC() which calculates purchase price

- Implementation Tip:

For precise institutional calculations:

=ROUND(RECEIVED(…), 2)

Related Functions

- PRICEDISC(): Calculates purchase price from face value

- YIELDDISC(): Determines equivalent yield

- INTRATE(): Calculates the interest rate