Its calculates straight-line depreciation for an asset over a specified period, allocating equal depreciation expense in each accounting period.

Syntax

SLN(Cost; Salvage; Life)

Arguments

| Argument | Required | Description | Validation Rules |

| Cost | Yes | Initial asset value (purchase price + incidental costs) | Must be positive |

| Salvage | Yes | Asset value at end of depreciation | Must be ≥ 0 |

| Life | Yes | Useful life in periods | Must be integer > 0 |

Error Conditions

- #VALUE!: Non-numeric inputs

- #NUM!: Negative values or invalid Life

Calculation Method

Annual Depreciation = (Cost – Salvage) / Life

Key Features

- Equal Periodic Charges: Allocates depreciation evenly across all periods

- Common Applications:

- Financial reporting

- Tax calculations (where permitted)

- Budget forecasting

Example

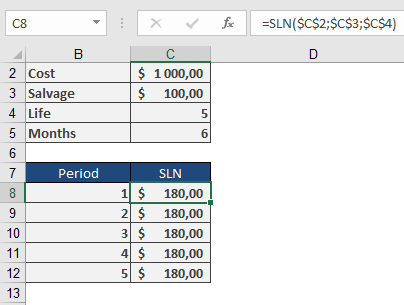

Asset Depreciation Scenario:

- Purchase cost: $1,000

- Salvage value: $100

- Useful life: 5 years

Calculation:

=SLN(1000, 100, 5)

Result: $180 per year

Depreciation Schedule:

| Year | Beginning Value | Depreciation | Ending Value |

| 1 | $1,000 | $180 | $820 |

| 2 | $820 | $180 | $640 |

| 3 | $640 | $180 | $460 |

| 4 | $460 | $180 | $280 |

| 5 | $280 | $180 | $100 |

Implementation Notes

- First-Year Convention:

- For partial-year depreciation, manually adjust first period

- Use SLN() for subsequent full periods

- Best Practices:

=ROUND(SLN(Cost, Salvage, Life), 2)

Ensures compliance with financial reporting standards

- Complementary Functions:

- DB(): Declining balance method

- DDB(): Double-declining balance

- SYD(): Sum-of-years’ digits

Technical Considerations

- Tax Compliance:

- Verify local regulations permit straight-line method

- Some jurisdictions require accelerated methods

- Asset Management:

- Combine with physical depreciation tracking

- Useful for capital budgeting analysis