Its Calculates the bond-equivalent yield (annualized return) for a U.S. Treasury bill (T-bill) based on its discount rate, converting the T-bill’s discount yield (360-day basis) to an equivalent investment yield (365-day basis).

Syntax

TBILLEQ(Settlement; Maturity; Discount)

Arguments

| Argument | Required | Description | Validation Rules |

| Settlement | Yes | Trade date (when T-bill is purchased). | Must be a valid date < Maturity. |

| Maturity | Yes | Maturity date (when T-bill is redeemed). | Must be ≤ 1 year after Settlement. |

| Discount | Yes | Discount rate (as a decimal, e.g., 5% = 0.05). | Must be > 0. |

Error Conditions

- #VALUE!: Invalid dates.

- #NUM!: If:

- Settlement ≥ Maturity

- Maturity > 1 year after Settlement

- Discount ≤ 0

Background

T-bills are zero-coupon securities sold at a discount and redeemed at par. The TBILLEQ function converts the discount rate (used to price T-bills) into an equivalent annual yield (used to compare returns with other investments).

Key Formula

Where:

- Days = Actual days between Settlement and Maturity.

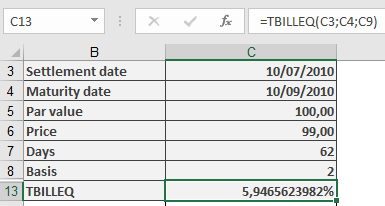

Example

Key Notes

- Comparison with Other Functions

- YIELDDISC(): Returns the yield directly (no 365-day conversion).

- RECEIVED(): Calculates maturity value, not yield.

- Practical Use

- Compare T-bill returns with bonds or savings accounts.

- Adjusts for the 360-day banking year used in T-bill pricing.

- Limitations

- Only valid for T-bills with maturities ≤ 1 year.

- Does not account for compounding.