Its calculates the annual yield of a discounted security (e.g., Treasury bills or commercial paper) that pays no periodic interest but is issued at a discount and redeemed at face value.

Syntax

YIELDDISC(Settlement; Maturity; Price; Redemption; [Basis])

Arguments

| Argument | Required | Description | Validation Rules |

| Settlement | Yes | Purchase date of the security. | Must be valid date < Maturity. |

| Maturity | Yes | Maturity/redemption date. | Must be valid date > Settlement. |

| Price | Yes | Purchase price per $100 face value. | Must be positive and < Redemption. |

| Redemption | Yes | Redemption value per $100 face value. | Typically 100. |

| [Basis] | No | Day-count convention (0-4). Default=0. | See Table 15-2. |

Error Conditions

- #VALUE!: Invalid dates.

- #NUM!: If:

- Price ≤ 0 or ≥ Redemption

- Settlement ≥ Maturity

- Basis ∉ {0,1,2,3,4}

Key Formula

Where:

- Days_in_Year: 360 (Basis=0,2,4) or 365 (Basis=1,3).

- Days_to_Maturity: Actual calendar days between Settlement and Maturity.

Examples

- Bill of Exchange (Supplier Loan)

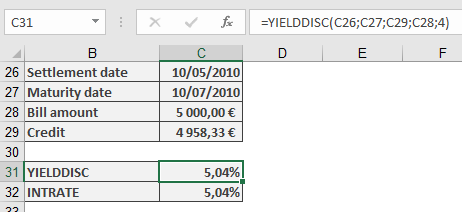

Scenario:

- Face Value: $5,000

- Purchase Price: $4,958.33 (5% discount)

- Settlement: 10-May-2010

- Maturity: 10-Jul-2010 (61 days)

- Basis: 4 (European 30/360)

Calculation:

=YIELDDISC(« 5/10/2010 », « 7/10/2010 », 4958.33, 5000, 4)

Result: 5.04% annual yield.

Background

- Discount vs. Yield:

- Discount Rate: Anticipative interest (applied upfront).

- Yield: Equivalent interest-in-arrears return.

- Day-Count Conventions:

| Basis | Method | Year Days |

| 0 | US (NASD) 30/360 | 360 |

| 1 | Actual/actual | 365/366 |

| 2 | Actual/360 | 360 |

| 3 | Actual/365 | 365 |

| 4 | European 30/360 | 360 |

- Comparison with RECEIVED():

- YIELDDISC() solves for yield given price.

- RECEIVED() solves for maturity value given yield.