Votre panier est actuellement vide !

Catégorie : Excel function

How to use the VDB() function in Excel

Its Calculates depreciation for an asset using the declining balance method, with an optional switch to straight-line depreciation when advantageous. This flexible approach is commonly used for tax purposes.

Syntax

VDB(Cost; Salvage; Life; Start_Period; End_Period; [Factor]; [No_Switch])

Arguments

Argument Required Description Validation Rules Cost Yes Initial asset value (purchase price + expenses). Must be positive. Salvage Yes Asset value at end of depreciation. Must be ≥ 0 and < Cost. Life Yes Useful life in periods (integer). Must be > 0. Start_Period Yes Starting period for depreciation calculation. Must be < Life. End_Period Yes Ending period for depreciation calculation. Must be ≥ Start_Period. [Factor] No Accelerated depreciation rate (default=2 for double-declining). Typically 1.5–2. [No_Switch] No FALSE (default): Switches to straight-line when optimal; TRUE: Forces declining balance. Logical (TRUE/FALSE). Error Conditions

- #VALUE!: Non-numeric inputs.

- #NUM!: If:

- Cost ≤ 0 or Salvage < 0

- Life ≤ 0 or Start_Period ≥ Life

- Factor ≤ 0

Background

The Variable Declining Balance (VDB) method combines:

- Accelerated Depreciation: Higher expenses in early years (e.g., double-declining balance).

- Automatic Switch to Straight-Line: When straight-line depreciation exceeds the declining balance amount.

Key Formula

Depreciation=Book Value×(FactorLife)Depreciation=Book Value×(LifeFactor)

- Book Value = Cost – Accumulated Depreciation.

- Switch Condition: If straight-line depreciation > declining balance, VDB switches.

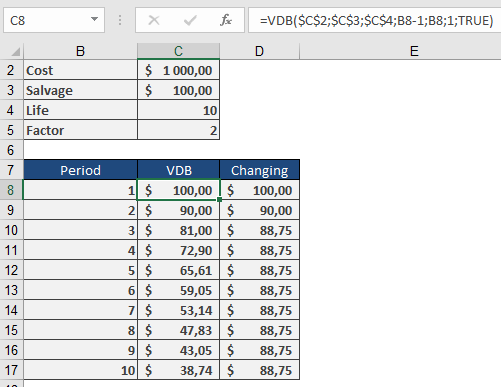

Example

Asset Depreciation:

- Cost: $1,000

- Salvage: $100

- Life: 10 years

- Factor: 2 (double-declining)

- No_Switch: FALSE (auto-switch enabled)

Depreciation Schedule

Year Method Depreciation Book Value 1 Double-Declining $200.00 $800.00 2 Double-Declining $160.00 $640.00 3 Double-Declining $128.00 $512.00 4 Straight-Line* $103.00 $409.00 … … … … *Switches to straight-line in Year 4 when it becomes more beneficial.

Key Features

- Tax Optimization: Maximizes early-year deductions.

- Flexibility: Adjust Factor for local tax rules (e.g., 1.5× for mid-range acceleration).

- Partial Periods: Combine with manual adjustments for mid-year purchases.

Complementary Functions

- DB(): Fixed declining balance (no switch).

- DDB(): Double-declining balance (no switch).

- SLN(): Straight-line depreciation.

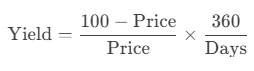

How to use the TBILLYIELD() function in Excel

Its calculates the yield to maturity of a U.S. Treasury bill (T-bill) as an annualized percentage, based on the purchase price and time to maturity.

Syntax

TBILLYIELD(Settlement; Maturity; Price)

Arguments

Argument Required Description Validation Rules Settlement Yes Trade settlement date (purchase date). Must be valid date < Maturity. Maturity Yes Maturity/redemption date. Must be ≤ 1 year after Settlement. Price Yes Purchase price per $100 face value. Must be positive and < 100 (discounted). Error Conditions

- #VALUE!: Invalid date format.

- #NUM!: If:

- Settlement ≥ Maturity

- Maturity > 1 year after Settlement

- Price ≤ 0 or ≥ 100

Background

T-bills are zero-coupon securities sold at a discount. The yield represents the annualized return if held to maturity.

Key Formula

Where:

- Days = Actual calendar days between Settlement and Maturity.

- Uses 360-day year (consistent with U.S. banking conventions).

Example

T-Bill Investment:

Key Notes

- Comparison with Other Functions

- YIELDDISC(Basis=2) matches TBILLYIELD().

- RECEIVED() calculates maturity value, not yield.

- Practical Use

- Compare T-bill returns with other short-term investments.

- Adjusts for the 360-day banking year (no compounding).

- Limitations

- Only valid for T-bills with maturities ≤ 1 year.

- Price must be < 100 (discounted securities).

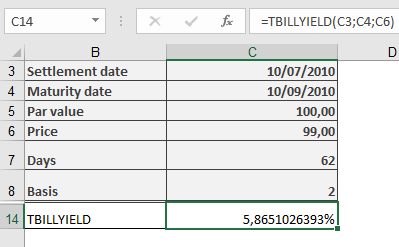

How to use the TBILLPRICE() function in Excel

Its calculates the price per $100 face value of a U.S. Treasury bill (T-bill) based on its discount rate. T-bills are short-term securities that are issued at a discount and mature at par value.

Syntax

TBILLPRICE(Settlement; Maturity; Discount)

Arguments

Argument Required Description Validation Rules Settlement Yes The trade settlement date Must be valid date < Maturity Maturity Yes The maturity/redemption date Must be ≤ 1 year after Settlement Discount Yes The annual discount rate (decimal) Must be > 0 Error Conditions

- #VALUE!: Invalid date format

- #NUM!: If:

- Settlement ≥ Maturity

- Maturity > 1 year after Settlement

- Discount ≤ 0

Calculation Method

The price is calculated using:

Price = 100 × (1 – Discount × D/360)

Where:

- D = Number of days between Settlement and Maturity

- Uses actual calendar days (Basis = 2 equivalent)

Example

Key Features

- Day Count Convention: Uses actual/360 (Basis = 2)

- Output Format: Returns price as percentage of par value

- Complementary Functions:

- TBILLYIELD(): Calculates yield from price

- PRICEDISC(): Similar but allows different day count bases

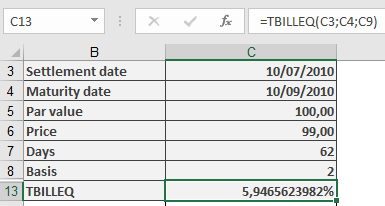

How to use the TBILLEQ() function in Excel

Its Calculates the bond-equivalent yield (annualized return) for a U.S. Treasury bill (T-bill) based on its discount rate, converting the T-bill’s discount yield (360-day basis) to an equivalent investment yield (365-day basis).

Syntax

TBILLEQ(Settlement; Maturity; Discount)

Arguments

Argument Required Description Validation Rules Settlement Yes Trade date (when T-bill is purchased). Must be a valid date < Maturity. Maturity Yes Maturity date (when T-bill is redeemed). Must be ≤ 1 year after Settlement. Discount Yes Discount rate (as a decimal, e.g., 5% = 0.05). Must be > 0. Error Conditions

- #VALUE!: Invalid dates.

- #NUM!: If:

- Settlement ≥ Maturity

- Maturity > 1 year after Settlement

- Discount ≤ 0

Background

T-bills are zero-coupon securities sold at a discount and redeemed at par. The TBILLEQ function converts the discount rate (used to price T-bills) into an equivalent annual yield (used to compare returns with other investments).

Key Formula

Where:

- Days = Actual days between Settlement and Maturity.

Example

Key Notes

- Comparison with Other Functions

- YIELDDISC(): Returns the yield directly (no 365-day conversion).

- RECEIVED(): Calculates maturity value, not yield.

- Practical Use

- Compare T-bill returns with bonds or savings accounts.

- Adjusts for the 360-day banking year used in T-bill pricing.

- Limitations

- Only valid for T-bills with maturities ≤ 1 year.

- Does not account for compounding.

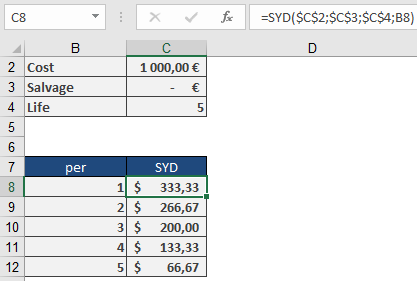

How to use the SYD() function in Excel

Its calculates the depreciation of an asset for a specified period using the sum-of-the-years’ digits (SYD) method, an accelerated depreciation technique that applies higher depreciation expenses in earlier periods.

Syntax

SYD(Cost; Salvage; Life; Per)

Arguments

Argument Required Description Validation Rules Cost Yes Initial asset cost (purchase price + additional expenses – discounts). Must be a positive value. #VALUE! if non-numeric, invalid if negative. Salvage Yes Asset value at the end of its useful life. Must be ≥ 0. #VALUE! if non-numeric, #NUM! if negative. Life Yes Total depreciation periods (integer > 0). Must be a positive integer. Per Yes Specific period for depreciation calculation (integer > 0). Must be ≤ Life. Background

Depreciation reflects the reduction in an asset’s value over time. The SYD method applies a declining depreciation expense each period, unlike straight-line depreciation.

Key Features

- Accelerated Depreciation: Higher expenses in early years, decreasing over time.

- Formula:

-

- Numerator: Remaining useful life at the start of the period.

- Denominator: Sum of the years’ digits (e.g., 5 years → 1+2+3+4+5 = 15).

- Tax & Accounting Use:

- Permitted in some jurisdictions for tax benefits.

- Not suitable for all assets (check local regulations).

Example

Asset Details:

- Cost: $1,000

- Salvage Value: $0

- Life: 5 years

Depreciation Schedule:

Year Calculation (SYD) Depreciation Book Value 1 =SYD(1000,0,5,1) $333.33 $666.67 2 =SYD(1000,0,5,2) $266.67 $400.00 3 =SYD(1000,0,5,3) $200.00 $200.00 4 =SYD(1000,0,5,4) $133.33 $66.67 5 =SYD(1000,0,5,5) $66.67 $0.00 Key Takeaway:

- Year 1 has the highest depreciation ($333.33).

- Year 5 has the lowest ($66.67).

Implementation Notes

- Partial-Year Depreciation:

- SYD assumes full periods. Adjust manually for mid-year purchases.

- Complementary Functions:

- SLN(): Straight-line depreciation.

- DDB(): Double-declining balance (more aggressive than SYD).

- Best Practices:

- Use ROUND(SYD(…), 2) for financial reporting precision.

- Verify tax compliance before applying SYD.

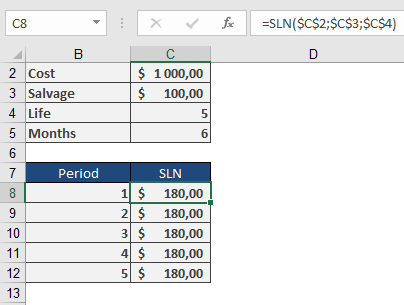

How to use the SLN() function in Excel

Its calculates straight-line depreciation for an asset over a specified period, allocating equal depreciation expense in each accounting period.

Syntax

SLN(Cost; Salvage; Life)

Arguments

Argument Required Description Validation Rules Cost Yes Initial asset value (purchase price + incidental costs) Must be positive Salvage Yes Asset value at end of depreciation Must be ≥ 0 Life Yes Useful life in periods Must be integer > 0 Error Conditions

- #VALUE!: Non-numeric inputs

- #NUM!: Negative values or invalid Life

Calculation Method

Annual Depreciation = (Cost – Salvage) / Life

Key Features

- Equal Periodic Charges: Allocates depreciation evenly across all periods

- Common Applications:

- Financial reporting

- Tax calculations (where permitted)

- Budget forecasting

Example

Asset Depreciation Scenario:

- Purchase cost: $1,000

- Salvage value: $100

- Useful life: 5 years

Calculation:

=SLN(1000, 100, 5)

Result: $180 per year

Depreciation Schedule:

Year Beginning Value Depreciation Ending Value 1 $1,000 $180 $820 2 $820 $180 $640 3 $640 $180 $460 4 $460 $180 $280 5 $280 $180 $100 Implementation Notes

- First-Year Convention:

- For partial-year depreciation, manually adjust first period

- Use SLN() for subsequent full periods

- Best Practices:

=ROUND(SLN(Cost, Salvage, Life), 2)

Ensures compliance with financial reporting standards

- Complementary Functions:

- DB(): Declining balance method

- DDB(): Double-declining balance

- SYD(): Sum-of-years’ digits

Technical Considerations

- Tax Compliance:

- Verify local regulations permit straight-line method

- Some jurisdictions require accelerated methods

- Asset Management:

- Combine with physical depreciation tracking

- Useful for capital budgeting analysis

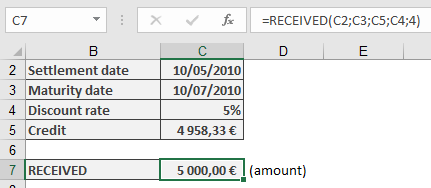

How to use the RECEIVED() function in Excel

Its calculates the maturity value (redemption amount) for a fully discounted security that uses anticipative interest calculation (interest deducted upfront).

Syntax

RECEIVED(Settlement; Maturity; Investment; Discount; [Basis])

Arguments

Argument Required Description Validation Rules Settlement Yes Trade settlement date Must be valid date ≤ Maturity Maturity Yes Security maturity date Must be valid date ≥ Settlement Investment Yes Amount invested (purchase price) > 0 Discount Yes Annual discount rate > 0 [Basis] No Day count convention (0-4) Default=0 Error Conditions

- #VALUE!: Invalid dates or non-numeric inputs

- #NUM!: Negative amounts or invalid Basis

Key Features

- Anticipative Interest Model:

- Interest deducted at inception (discount instrument)

- Contrasts with standard arrears interest calculation

- Common Applications:

- Treasury bills

- Commercial paper

- Bankers’ acceptances

Calculation Method

Maturity Value = Investment / (1 – (Discount × DSM/DIM))

Where:

- DSM = Days from settlement to maturity

- DIM = Days in year per Basis convention

Examples

- Bill of Exchange

Scenario:

- Settlement: 10-May-2010

- Maturity: 10-Jul-2010 (2 months)

- Investment: $4,958.33

- Discount: 5% p.a.

- Basis: 4 (European 30/360)

Calculation:

=RECEIVED(« 5/10/2010″, »7/10/2010 »,4958.33,5%,4)

Result: $5,000.00

Face value of the billImportant Notes

- Day Count Conventions:

Basis Method 0 US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 - Financial Context:

- Primarily for short-term instruments (<1 year)

- Represents the face value calculation

- Complementary to PRICEDISC() which calculates purchase price

- Implementation Tip:

For precise institutional calculations:

=ROUND(RECEIVED(…), 2)

Related Functions

- PRICEDISC(): Calculates purchase price from face value

- YIELDDISC(): Determines equivalent yield

- INTRATE(): Calculates the interest rate

How to use the RATE() function in Excel

Its calculates the periodic interest rate for a loan or investment based on constant periodic payments and/or a lump sum amount.

Syntax

RATE(Nper; Pmt; Pv; [Fv]; [Type]; [Guess])

Arguments

Argument Requirement Description Financial Context Nper Required Total number of periods Loan term/investment horizon Pmt Conditionally Required Payment per period Annuity amount Pv Conditionally Required Present value Loan principal/initial investment [Fv] Optional Future value Target balance/residual value [Type] Optional Payment timing:

0 = end period (default)

1 = beginning periodCash flow timing [Guess] Optional Starting guess for iterative calculation (default=10%) Initial estimate Note: Either Pmt or Fv must be provided.

Calculation Method

Uses iterative approximation to solve the time value of money equation:

Pv + Σ[Pmt/(1+Rate)^k] + Fv/(1+Rate)^Nper = 0

where k ranges from 1 to Nper (adjusted for Type).

Key Applications

- Investment Yield Analysis

- Loan Interest Determination

- Annuity Rate Calculation

- Capital Budgeting (IRR alternative)

Examples

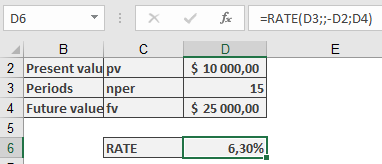

- Retirement Savings Target

Scenario:

$10,000 growing to $25,000 in 15 years.Calculation:

=RATE(15,,-10000,25000)

Result: 6.3% p.a.

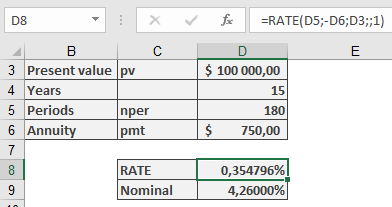

Required annual return to meet goal.- Pension Annuity Funding

Scenario:

$100,000 fund providing $750/month for 15 years (payments at start of month).Calculation:

=RATE(15*12,-750,100000,,1)

Result: 0.3548% monthly (4.26% p.a.)

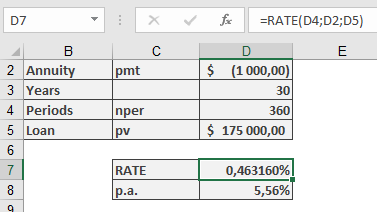

Required monthly compounding rate.- Mortgage Pricing

Scenario:

$175,000 loan with $1,000 monthly payments over 30 years.Calculation:

=RATE(30*12,-1000,175000)

Result: 0.4632% monthly (5.56% p.a.)

Effective annual interest rate.Technical Notes

- Iterative Process:

- Begins with Guess value (default 10%)

- Uses Newton-Raphson approximation

- May fail to converge if no solution exists

- Complementary Functions:

- IRR(): For irregular cash flows

- XIRR(): For irregular dates

- NPER(): For term calculations

- Financial Best Practices:

- For monthly results, multiply by 12 for APR

- Use negative values for cash outflows

- Combine with ROUND() for presentation:

=ROUND(RATE(…)*12,2)& »% p.a. »

How to use the PV() function in Excel

Its calculates the present value of an investment based on a constant interest rate and a series of future payments (annuities) and/or a lump sum.

Syntax

PV(Rate; Nper; [Pmt]; [Fv]; [Type])

Arguments

Argument Requirement Description Financial Meaning Rate Required Interest rate per period Cost of capital/discount rate Nper Required Total number of periods Investment/loan term [Pmt] Conditionally Required Payment per period Annuity amount [Fv] Optional Future value Target balance/residual value [Type] Optional Payment timing:

0 = end period (default)

1 = beginning periodCash flow timing Note: Either Pmt or Fv must be provided.

Financial Model

Implements the time value of money principle:

PV + Σ[Pmt/(1+Rate)^k] + Fv/(1+Rate)^Nper = 0

where k ranges from 1 to Nper (adjusted for Type).

Key Applications

- Lump Sum Investments (Retirement Planning)

=PV(Rate, Nper,, Fv)

- Annuity Valuation (Pension Planning)

=PV(Rate, Nper, Pmt)

- Loan Capacity (Mortgage Underwriting)

=PV(Rate, Nper, -Pmt)

Examples

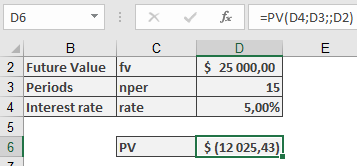

- Retirement Savings Verification

Scenario:

$10,000 invested for 15 years at 5% p.a. targeting $25,000.Calculation:

=PV(5%, 15,, 25000)

Result: -$12,025.43

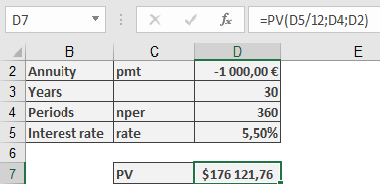

Interpretation: Requires $12,025 initial investment to reach target (current $10,000 insufficient).- Mortgage Qualification

Scenario:

$1,000 monthly payment capacity for 30 years at 5.5% p.a.Calculation:

=PV(5.5%/12, 30*12, -1000)

Result: $176,121.76

Interpretation: Maximum loan amount at given terms.Important Notes

- Sign Convention:

- Positive results = Cash inflows

- Negative results = Cash outflows

- Compounding Assumptions:

- For monthly payments, divide annual rate by 12

- For quarterly payments, divide annual rate by 4

- Precision Tip:

For loan amortization schedules, combine with ROUND():

=ROUND(PV(…), 2)

How to use the PRICEMAT() function in Excel

Its calculates the price per 100 currency units of face value for a security that pays simple interest at maturity (no compounding).

Syntax

PRICEMAT(Settlement; Maturity; Issue; Rate; Yield; [Basis])

Arguments

Argument Requirement Description Validation Rules Settlement Required Trade date Must be valid date < Maturity maturity Required Maturity date Must be valid date > Settlement issue Required Security issuance date Must be valid date ≤ Settlement rate Required Annual coupon rate ≥ 0 yield Required Annual market yield ≥ 0 [basis] Optional Day count convention (0-4) Default=0 Error Conditions

- #VALUE!: Invalid dates

- #NUM!: Negative rates/yields or Basis ∉ {0,1,2,3,4}

Key Features

- Simple Interest Model:

- Interest calculated linearly (no compounding)

- Appropriate for short-term instruments

- Price Components:

- Principal repayment at maturity

- Full-term interest payment

- Discounted at market yield

Calculation Method

Price = [Repayment + (Rate × DIM/YearDays)] / (1 + Yield × DSM/YearDays) – Accrued Interest

Where:

- DIM = Days from issue to maturity

- DSM = Days from settlement to maturity

- YearDays = Days in year per Basis

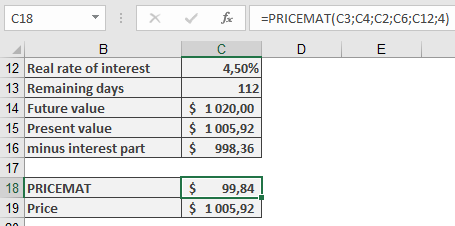

Example

Important Notes

- Day Count Conventions:

- 0 = US (NASD) 30/360

- 1 = Actual/actual

- 2 = Actual/360

- 3 = Actual/365

- 4 = European 30/360

- Financial Applications:

- Commercial paper

- Short-term notes

- Certificates of deposit

- Complementary Functions:

- ACCRINT(): Calculates accrued interest

- YIELDMAT(): Determines equivalent yield

- Implementation Tip:

For precise institutional calculations:

=ROUND(PRICEMAT(…),2) + ROUND(ACCRINT(…),2)